Russia's Coal Industry After 2022

The Hidden Costs of Putinism’s Extractive Model

Analytical Review | May 2026

TABLE OF CONTENTS

I SANCTIONS AND COAL EXPORTS

II RAIL FREIGHT SUBSIDIES ARE THE BASIS OF COAL EXPORTS

III COAL LOBBY IN THE MINISTRY OF ENERGY

IV ENVIRONMENTAL AND CLIMATE IMPACTS

V STATE-CAPTURED EXTRACTIVIST SUBSIDY REGIME

IN THE COAL INDUSTRY

VI METHANE EMISSIONS IN RUSSIA: AN UNDERESTIMATED CLIMATE RISK

Author: Anton Lementuev

Key findings

-

Russia’s coal industry did not collapse after 2022, but it lost its sustainable economic model.

-

The EU coal embargo forced Russian exporters to redirect supplies to Asia, but Asian markets did not restore previous profitability.

-

China helped preserve Russian export volumes, but it did not become a full replacement for the European market.

-

Russian coal exports depend heavily on hidden state support, including rail freight subsidies, export quotas, tax concessions and weakened oversight.

-

Open-pit coal mining has become the dominant extraction method in Russia, intensifying landscape degradation, waste generation and dust pollution.

-

Russian methane and greenhouse gas reporting should not be accepted without independent external verification.

About the report

Russia’s coal industry did not collapse after the start of the full-scale war against Ukraine, but it lost its sustainable economic model. The EU coal embargo deprived Russian exporters of a premium market and forced the industry to redirect exports to Asia. In physical terms, this adaptation partly worked: Russia continued to produce and export large volumes of coal. Economically, however, the sector entered a deep crisis.

This analytical review examines Russia’s coal industry after 2022 as a model case of a wider problem: the survival of an export-oriented raw-materials economy under war, sanctions, state support and weakened environmental regulation. The report focuses on coal exports and logistics, dependence on China and other Asian markets, rail freight subsidies, equipment supply chains, the environmental consequences of open-pit coal mining, and the reliability of Russian methane and climate reporting.

Executive summary

Russia’s coal industry has remained physically large but economically weakened. In 2025, Russia produced approximately 440–443 million tonnes of coal and exported about 211 million tonnes, remaining one of the world’s largest coal exporters. However, maintaining production and export volumes no longer means financial stability. By 2024–2025, the export model had entered a state of crisis.

The consolidated net loss of Russian coal companies reached approximately USD 5.3 billion in 2025

Cumulative industry losses since 2022 can be estimated at more than USD 32 billion. Exports to China, India, Turkey and South Korea helped preserve shipment volumes, but they did not restore profitability.

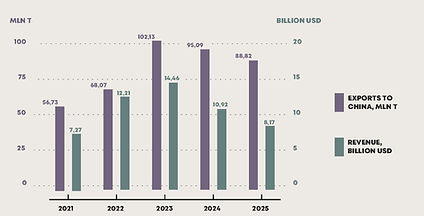

China became the main destination for Russian coal after the loss of the European market, but it has not become a full replacement for Europe. Russia’s share of China’s coal imports never exceeded 24% even at its peak and stood at around 18% in 2025.

Average revenue from Russian coal deliveries to China declined from USD 142 per tonne in 2023 to USD 92 per tonne in 2025.

The main competitive advantage of Russian coal is not efficiency, but a system of hidden subsidies. Coal mining accounts for less than 1% of Russia’s GDP, yet coal represents approximately 28–29% of all freight loaded onto the Russian Railways network.

Over 10 years, Russian Railways’ losses from coal transportation reached USD 5.64 billion, while profits from transporting oil cargoes totaled USD 5.9 billion.

Without artificially reduced rail tariffs, administratively guaranteed export quotas and tax relief, a substantial share of Russian coal exports would be economically unviable.

Sanctions also disrupted supplies of mining equipment. After the withdrawal of Western manufacturers, China, Turkey and countries of the Eurasian Economic Union became key alternative supply channels. Kazakhstan is particularly illustrative: exports of specialised machinery from Kazakhstan to Russia increased from approximately USD 1 million in 2021 to USD 36.5 million in 2024.

According to the Russian Ministry of Energy, the coal industry is approximately 80% dependent on imported machinery

The crisis has hit Kuzbass, Russia’s main coal-producing and coal-exporting region. Corporate profit tax revenues to the Kuzbass regional budget fell sharply, while coal companies increased layoffs. At the same time, regional payments for signing contracts with the Ministry of Defence and deployment to the war against Ukraine were reduced almost fourfold.

Approximately 70% of the industry’s total losses were recorded in Kemerovo Region.

The environmental costs of Russian coal remain largely externalised: they are kept off corporate balance sheets and are not reflected in market prices. In 2023, the coal industry generated approximately 6 billion tonnes of waste — the highest level documented in the available official data. In 2024, the officially reported decline in waste volumes reflected not genuine environmental improvement, but changes in the accounting rules for overburden and host rock.

More than 78% of coal in Russia is produced through open-pit mining — the cheapest and most environmentally destructive extraction method.

Coal companies keep their costs low by shifting pollution, cleanup costs, health risks and resettlement expenses onto local residents, the state and the environment.

Russia’s state-captured extractivist subsidy regime is a hidden form of

support for extractive industries in which part of the costs of resource

extraction, processing and transportation is shifted from subsoil users

to residents of affected territories, local ecosystems and future public

expenditure. Weak regulation, regulatory inaction and the dependence

of oversight bodies on the industries they are supposed to supervise

allow these costs to be shifted away from extractive companies.

The climate impact of Russian coal mining is also not accurately reflected in international reporting. Russia is one of the world’s largest sources of methane, but estimates vary widely. Russia’s national greenhouse gas inventory reports about 9 million tonnes of CH4 per year, while the International Energy Agency estimates methane emissions from oil, gas and coal alone at around 14 million tonnes of CH4 annually.

In 2024–2025, Russia introduced a new “sovereign” methodology that reduced estimated net greenhouse gas emissions by roughly 30%, mainly through revised calculations of forest absorption capacity and lower estimates of industrial emissions.

Photo 1. Man-made landscapes and coal mine spoil heaps within the city limits of Kiselevsk, Kuzbass.

Figure 1. Trends in Russian coal exports to China and export revenues, 2021–2025

Photo 2. Open-pit coal mining at the Bachatsky open-pit coal mine in Kuzbass.

Photo: Alisa Nikulina

Figure 1. Selected methane super-emission events at coal industry facilities in Kuzbass based on Carbon Mapper data.

The Green Think Tank is a community of experts dedicated to analyzing the current situation in Russia and designing green reforms for the future. We are convinced that environmental transformation is an economic and political imperative for a more resilient future for Russia and beyond.

We are open to your questions and collaboration ideas. Please get in touch with us.

greenthinktank.life@proton.me